- MMR, on the other hand, saw a dip – from $574 Mn in 9M FY22 to $224 Mn in 9M FY23

- Chennai also saw increased PE action – from $37 Mn in 9M FY22 to approx. $268 Mn in 9M FY23

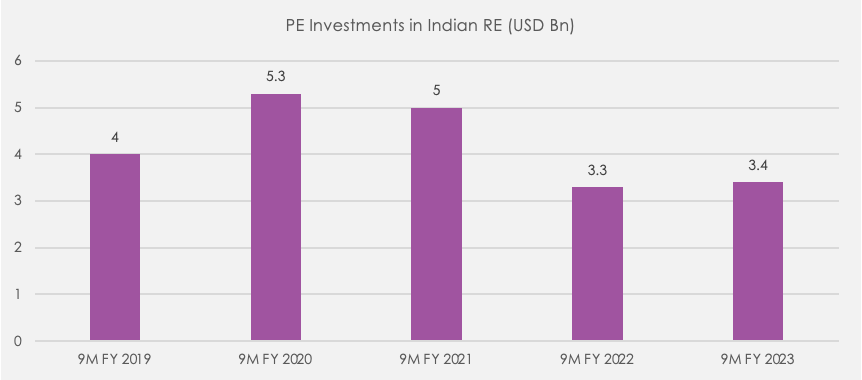

- Overall, Indian real estate attracted $3.4 Bn in 9M FY23 against approx. $3.3 Bn in this period in FY22, rising by 3%

- Top 10 deals alone accounted for 76% of total PE funding value in 9M FY23, compared to 72% in 9M FY22

- Average ticket size increased from $82 Mn in 9M FY22 to $91 Mn in 9M FY23

Mumbai, 10 January 2023: The Covid-19 pandemic was no deterrent for the NCR real estate market, which remained vibrant and performed remarkably well in 2022. The region witnessed more interest from private equity players than its counterpart realty hotspot MMR.

ANAROCK Capital’s Flux – 9M FY23 report reveals that PE players invested USD 1,215 Mn into NCR the in first nine months (9M) of FY23, against USD 771 Mn in the corresponding period in the previous financial year. This was a 58% yearly jump in total PE inflows in the region.

The report finds that MMR witnessed a drop in total inflows during the period – from USD 574 Mn in 9M FY22 to USD 224 Mn in 9M FY23. Investor focus has shifted visibly. Interestingly, Chennai, which accounted for a mere 1% share of total PE inflows in 9M FY22, saw its share rise to 8% in 9M FY23. As much as USD 268 Mn were invested in Chennai in 9M FY23, against USD 37 Mn in 9M FY22.

Overall, Indian real estate attracted USD 3.4 Bn of PE funding in 9M FY23, against USD 3.3 Bn in the corresponding period in FY22 – an annual increase of 3%.

The top 10 deals alone accounted for 76% of the total value of PE investments in 9M FY23, compared to 72% in 9M FY22. The average deal ticket size rose from USD 82 MN in 9M FY22 to USD 91 MN in 9M FY23.

Top 10 PE Deals in 9M FY23

| Capital Provider | Recipient | Location | Asset Class | Deal Amount (USD Mn) | Debt or Equity |

| CPPIB | TRIL | Multiple | Commercial | 700 | Equity |

| Brookfield | Bharti Enterprises | NCR | Commercial | 660 | Equity |

| HDFC Capital Advisors | Shapoorji Pallonji | Multiple | Residential | 194 | Debt |

| Axis AMC | Tishman Speyer | Multiple | Commercial | 188 | Equity |

| CapitaLand Investment | CapitaLand Development | Chennai | Commercial | 177 | Equity |

| Bain Capital | TARC (Anant Raj) | NCR | Residential | 175 | Debt |

| Brookfield | IL&FS | MMR | Commercial | 137 | Equity |

| Brookfield | L&T Metro Rail(Larson & Toubro) | Hyderabad | Land | 129 | Equity |

| Credit Suisse | Adani Properties | Multiple | Mixed Use | 101 | Debt |

| Blackstone | Vertical Warehousing | NCR | Logistics & Warehousing | 88 | Equity |

Shobhit Agarwal, MD & CEO – ANAROCK Capitals, says, “With a rise in the hybrid work model and corporates expanding into tier 2 cities for their ease of working, demand and confidence in the commercial space has resurged. Confidence in the residential sector is also high currently, and will remain constant on the back of strong continued homeownership sentiment.”

“In the retail segment, PE investments have remained subdued but are expected to gain momentum with physical shopping levels returning,” he says. “Thanks to the buoyant manufacturing sector, favourable government policies and the booming 3PL sector, high momentum is expected in the Industrial & Logistics sector in the future.”

Other Key Highlights

- Equity vs Debt Funding: PE investors prefer equity investment, which is visible from the fact that its share continues to be a healthy 77%

- Asset Class-wise Funding: The commercial real estate sector has witnessed increased capital inflows via PE investments, accounting for the highest market share of 55% in 9M FY23 as compared to 33% in 9M FY22. This can be attributed to investors’ continued preference for Grade A office assets with quality tenants. As an aftermath of pandemic, demand in residential sector has resulted in it drawing the second-highest share of 23% in 9M FY23. The residential asset class has seen PE growing from 568 USD Mn in 9M FY22 to 772 USD Mn in 9M FY23.

- Domestic vs Foreign Funding: At 948 USD Mn, domestic investments increased to 61% of the total PE capital inflows in Indian real estate in 9M FY23, compared to 587 USD Mn in 9M FY22. Foreign investments have dropped to 71% in 9M FY23 compared to 78% in 9M FY22.

Also Read:

- PE inflows in India real estate up 19% in FY21, investors eye portfolio deals across cities

- Listed Developers’ Cost of Debt Dips to 8.14% in Q2 FY23 from 9.64% in Q4 FY20

- Real Estate PE Investments Log 40% Annual Rise in 1H FY23: Report

- Housing Sales in Top 7 Cities to Create New Peak in 2022, Breach Previous High of 2014

1 Comment