Mumbai, 14 April 2023 – Significant numbers of large real estate platform deals were announced in FY23, finds ANAROCK Capital’s FLUX FY23 Report. The platform deals worth $4.5 Bn was announced across real estate asset classes.

Shobhit Agarwal, MD & CEO – ANAROCK Capital, says, “Commercial real estate and Industrial & Logistics attracted Pan India platforms with larger deal values of over $500 Mn, while the residential sector attracted smaller ticket platform deals of between $50 Mn and $125 Mn, and these were largely regional in nature.”

Top 10 PE Deals in FY23

The top 10 deals accounted for 69% of the total value of PE investments.

Office assets dominated large ticket equity investments in FY23. Residential RE continued as an attractive destination for debt investments in FY23.

Share of Top 10 Deals

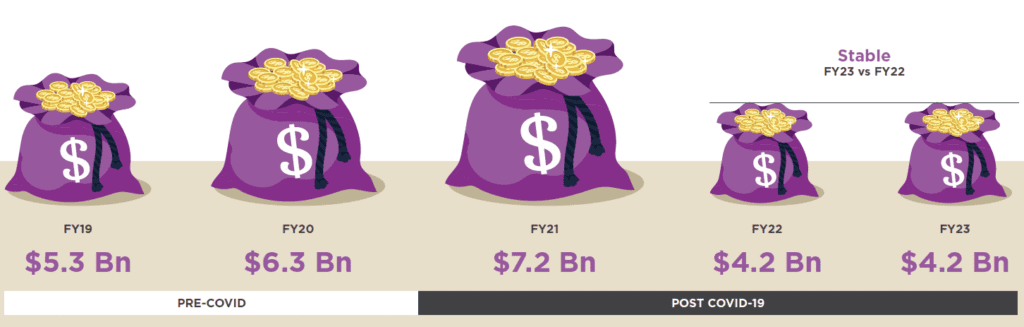

The top 10 deals accounted for 69% of the total value of PE investments in FY23 – largely stable compared to 67% in FY22.

Average Ticket Size

The average ticket size declined from $86 Mn in FY22 to $72 Mn in FY23. This is largely driven by increased activity in residential real estate, where deal sizes tend to be smaller.

Movement of Capital Inflow

NCR markets were a key attraction for PE players with 32% of total PE inflows in FY23, up from a share of 18% in FY22. Chennai accounted for 1% of total PE inflows in FY22 but increased its share to 8% of total PE inflows in FY23.

NCR, Chennai, Bengaluru & Hyderabad witnessed increased activity levels in FY23, while MMR, multi-city deals, and other cities witnessed lower activity levels than in FY22.

Equity vs Debt Funding

Equity investment is preferred by PE investors, visible from the fact that its share continues to be healthy at 67%. Increased activity in residential RE is reflected in higher share of debt at 33% in FY23 compared to 20% in FY22.

Asset Class-wise Funding

Commercial Office and the residential sectors continued to dominate PE activity respectively in FY23. Industrial & Logistics saw subdued activity post a robust FY22 and muted demand in FY23, especially from e-commerce players.

Domestic vs Foreign Funding

Domestic investors were significantly more active in FY23, with investment value increasing by 50% in FY23 ($0.9 Bn) over FY22 ($0.6 Bn). At the same time, foreign investors saw their incremental investments decline by 7% to $3.2 Bn in FY23, from $3.4 Bn in FY22. Consequently, the share of domestic PE investors in Indian RE increased from 14% in FY22 to 22% in FY23.

Key Takeaways

In FY23, there was a keen interest in platform deals, which generated a total deals value of $4.5 Bn.

Most of the large ticket platform deals were in rent-generating assets (offices & warehouses) for pan-India developments, while smaller ticket items were largely for residential developments in southern cities of India.

Offices continued to dominate the large ticket equity transactions, while residential projects continued to dominate debt instruments in FY23.

1. Commercial: The commercial office space saw a mixed bag with the IT sector, the largest driver of occupancy, facing uncertainty amidst global headwinds, impacting their expansion plans. The need to control costs and a yet-evolving hybrid workplace accentuated the uncertainty in near-term demand faced by office landlords. Bengaluru continued to dominate the India office market in supply & absorptions and average rentals remained flat-to-negative during FY23. An uptick in completions in FY24 amidst demand uncertainty is expected to keep rentals under pressure in FY24.

2. Residential: This sector continued its robust performance despite concerns of demand slowdown due to rate hikes. Sales & new launches continued to improve and developers took modest price hikes to cover cost inflation.

3. Industrial & Logistics: The I&L sector is at an inflection point and has seen tremendous growth over the years from being unorganized go-down structures to getting recognized as a prominent asset class. This sector is witnessing increased demand from 3PL, which we expect to sustain going forward into FY24.

However, the demand driver for FY22, e-commerce dragged in FY23 with players in the space not renewing their leases on expiry. The retail sector, which is being driven by a consumption boom amid rising disposable incomes and increased consumerism is expected to post steady performance in FY24. In terms of supply, new additions are likely to remain flat as lenders are wary of giving CF on speculative buildings.

4. Data Centres: FY23 witnessed major direct investments by hyper-scalers as India is expected to be a large data consumption and generation market in the next decade, making it strategically important in global operators’ APAC strategy. There is action on the ground with some large investments in land and the commitments are being deployed with the industry being focused on execution to ensure delivery to the large hyper-scalers.

6. Retail: Indian retail is in a sweet spot with consumption at malls well above pre-COVID levels. This is driving up demand for well-managed retail spaces, especially in tier-I cities. Given the robust consumer sentiment, investors are interested in acquiring quality retail assets which provide steady incomes and capital appreciation.

7. Alternatives: Investor interest is slowly rising into alternative asset classes like healthcare and life-sciences centers, co-living spaces, flexible office spaces, senior housing, etc.

See Also:

3 Comments